ROT and RUT work and VAT

The tax rebate for ROT and RUT work is intended for house or apartment owners and covers up to half of certain labour costs. After a customer has made payment to the company, the company then requests payment from the Tax Agency for the part of the labour costs which the customer has not paid, including VAT.

How must the invoice be structured?

For construction and engineering services, the Value Added Tax Act states that you must issue an invoice, even for sales to private people and those who are not traders.

- How an invoice must be structured is described in the Invoicing regulations for VAT (in Swedish)

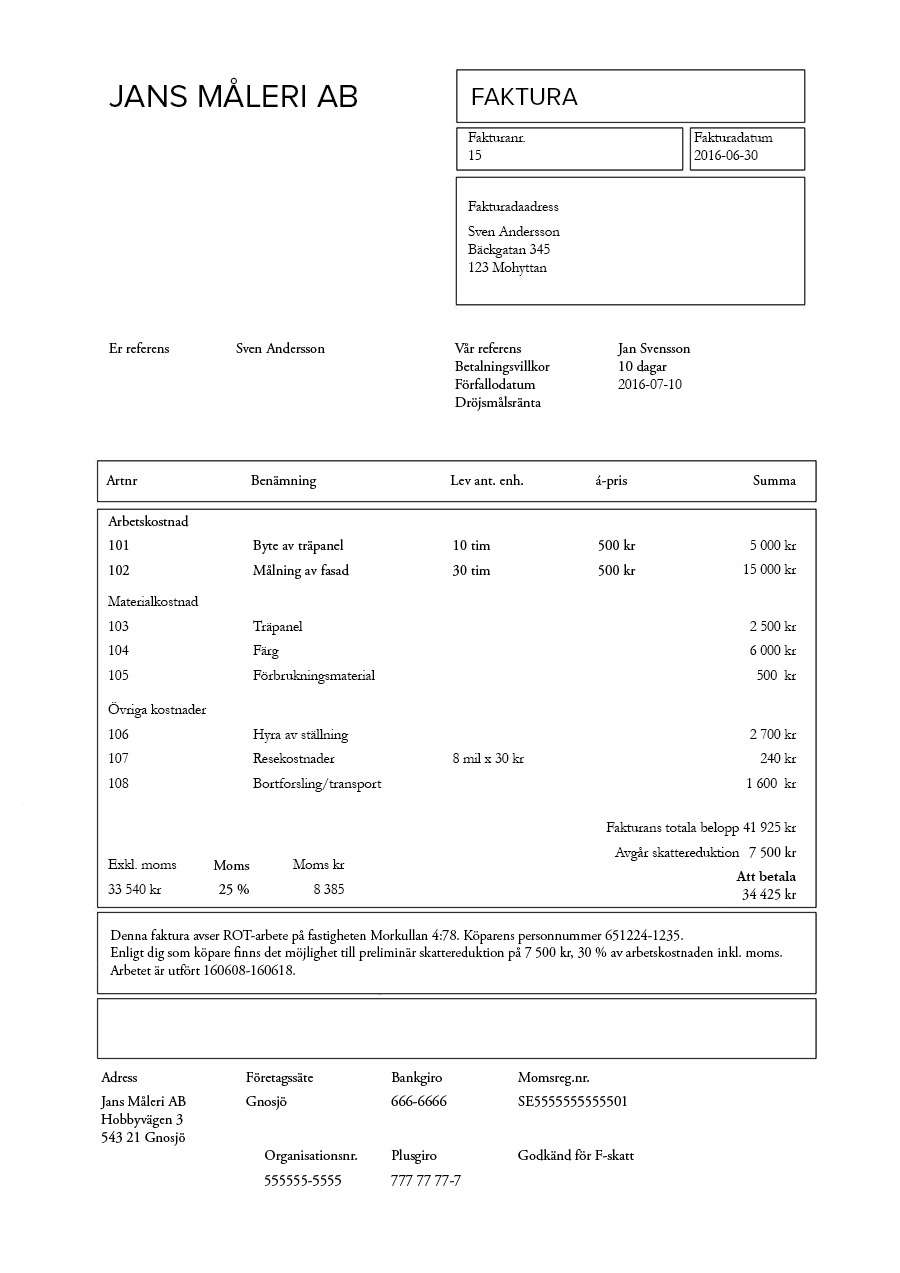

- Download the example invoice as an image (in Swedish) jpg, 143 kB.

{kind=link}

Invoice for ROT and RUT work

Even though there is no obligation to issue an invoice for the work you have carried out, under the Accounting Act you must still have some form of verification.

The following information must be included on an invoice:

- Who has carried out the work.

- Information that the provider pays company tax (F-skatt).

- The customer's civic registration number.

- The type of work that has been carried out.

- Where the work was performed and the time period.

- If it concerns ROT work, the registered organisation number of the housing association and the apartment number where the work was performed must be stated.

- The allocation of costs into labour and materials and other costs (e.g. machine costs, travel costs, transport and picking from stock).

- The total invoice amount, excluding and including VAT, the amount of VAT and its percentage.

- The amount of tax rebate.

Remember to make an agreement with your purchaser on what applies if the Tax Agency rejects your request for payment.

An example of an invoice

An invoice that is covered by the tax reduction may be drawn up as per the example below (figures in SEK):

Type | Amount |

|---|---|

Labour cost | 10,000 |

Materials | 8,000 |

Amount excl. VAT | 18,000 |

VAT 25% | 4,500 |

Total | 22,500 |

|

|

Amount paid out by Swedish Tax Agency |

|

30 % of labour cost incl. VAT | − 3,750 |

Payout | 18,750 |

When should I report the output VAT?

Invoicing method

If you use the invoicing method for reporting VAT, you must report output VAT in the period when you issue the invoice.

Accounts method

If you use the accounts method for reporting VAT, you must report output VAT in the period when you are paid.

In the last accounting period for the fiscal year you must also report output VAT on unpaid receivables. In the return for the accounting period, when the customer pays, output tax must be reported corresponding to the customer's payment.

In the invoice example above, the company must therefore report SEK 3,750 (20% of SEK 18,750) when the customer pays. The tax for the remaining part must be reported in the return for the accounting period in which the payment is received for that part. In the example, the VAT for this part is SEK 750 (20% of SEK 3,750).